This NHS tax calculator helps you work out exactly how much money you’ll take home from your NHS salary in the 2025/26 tax year. Whether you’re a nurse, healthcare assistant, doctor, or any other NHS staff member, you can instantly see how Income Tax, National Insurance, NHS pension contributions, and student loan repayments affect your pay.

The calculator works for all four UK nations—England, Scotland, Wales, and Northern Ireland—and automatically applies the correct tax bands and pension rates for your region. Simply enter your salary or select your NHS pay band, and you’ll see a complete breakdown of your monthly and annual take-home pay within seconds.

All calculations use official 2025/26 thresholds from HMRC and NHS Employers, including the updated pension contribution tiers following the 3.6% Agenda for Change pay award.

Read Guide: NHS Pay Bands 2025/26

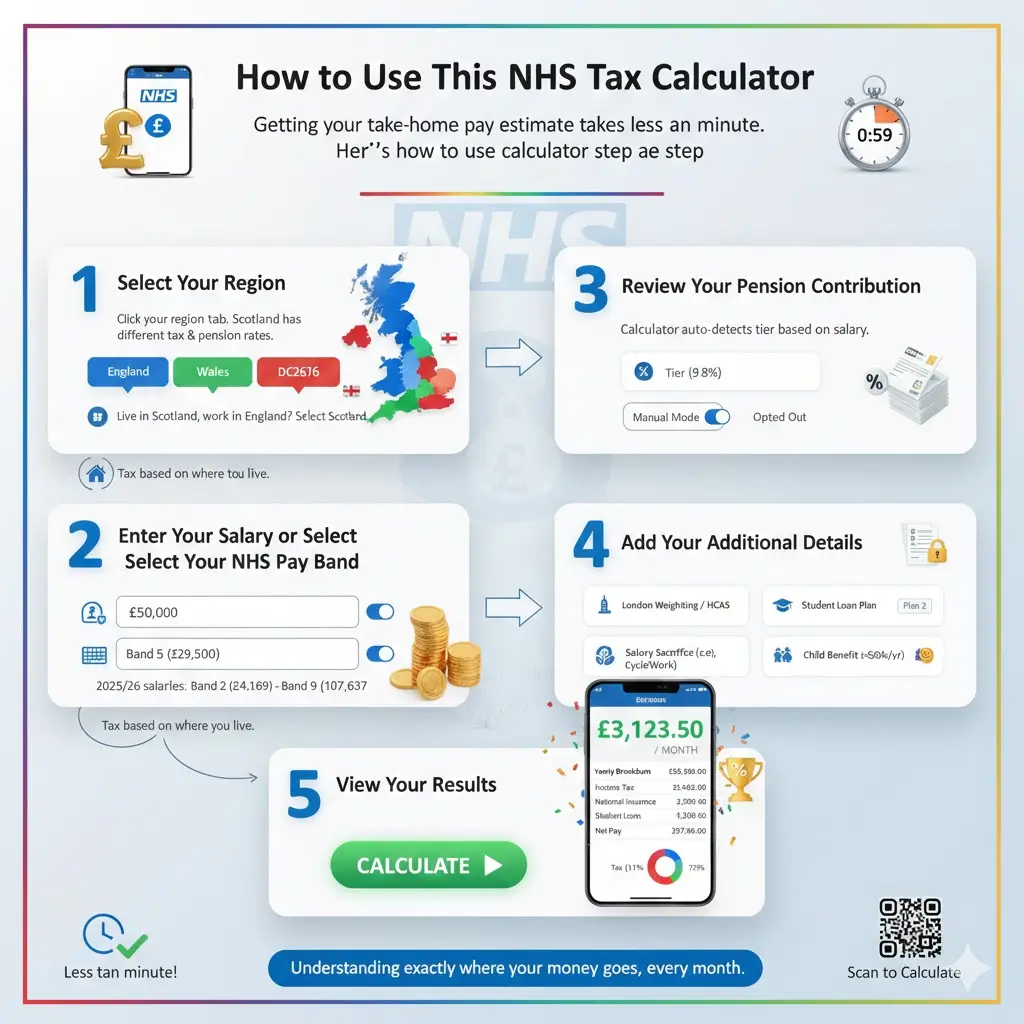

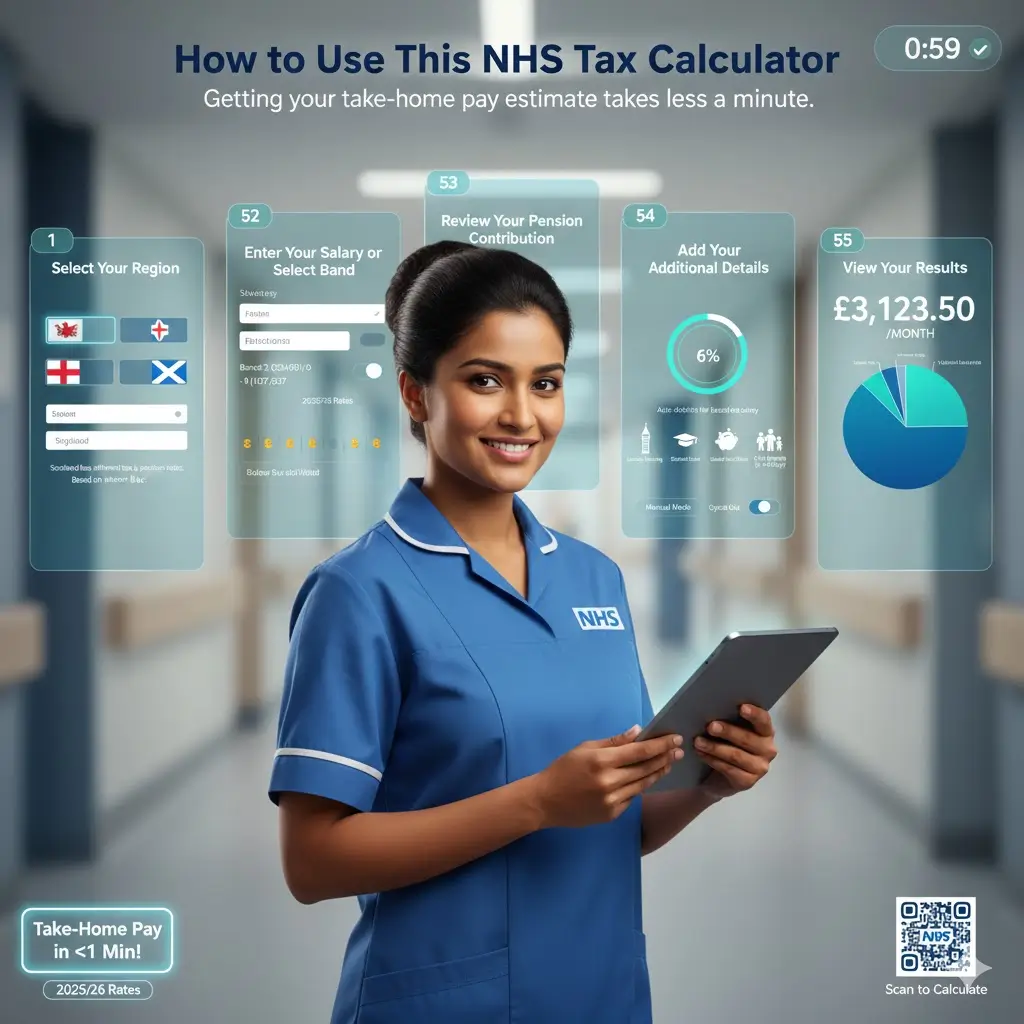

How to Use This NHS Tax Calculator

Getting your take-home pay estimate takes less than a minute. Here’s how to use the calculator step by step.

Step 1: Select Your Region

Start by clicking your region tab at the top—England, Scotland, Wales, or Northern Ireland. This matters because Scotland has its own income tax rates, and Scottish NHS staff also have different pension contribution tiers. If you work for an English NHS trust but live in Scotland, select Scotland because you pay tax based on where you live, not where you work.

Read Guide: NHS Band 5 Pay 2025/26

Step 2: Enter Your Salary or Select Your NHS Pay Band

You have two options here. You can type your exact annual salary if you know it, or you can toggle to “Select Band” and pick your Agenda for Change pay band. The calculator includes all 2025/26 starting salaries from Band 2 (£24,169) up to Band 9 (£107,637).

If you’re not sure of your exact salary, selecting your band gives you a quick estimate based on the starting point for that band.

Step 3: Review Your Pension Contribution

The calculator automatically works out your NHS pension tier based on your salary. You’ll see a small indicator showing which tier you fall into and the percentage rate. If your payslip shows a different rate, you can switch to manual mode and select your tier yourself. You can also choose “opted out” if you’ve left the pension scheme.

Step 4: Add Your Additional Details

Fill in any extras that apply to you:

-

- London weighting or HCAS if you work in a high cost area

-

- Student loan plan if you’re still repaying

-

- Salary sacrifice amounts for schemes like Cycle2Work or childcare

-

- Child benefit if you receive it and earn over £60,000

Step 5: View Your Results

Click calculate and you’ll see your monthly take-home pay as the headline figure. Below that, you get a full yearly breakdown showing exactly how much goes to tax, National Insurance, pension, and any other deductions. This helps you understand precisely where your money goes each month.

Read Guide: NHS Band 6 Pay 2025/26

Understanding Your NHS Tax Deductions in 2025/26

When you look at your NHS payslip, you’ll notice several deductions taken from your gross salary before you receive your take-home pay. Let’s break down what each one means and how it’s calculated.

Read Guide: NHS Band 7 Pay 2025/26

Income Tax for NHS Staff

Income tax is the biggest deduction for most NHS workers. Everyone gets a personal allowance of £12,570 per year—this is the amount you can earn completely tax-free. After that, you pay tax at different rates depending on how much you earn.

For NHS staff in England, Wales, and Northern Ireland, the rates are straightforward. You pay 20% basic rate tax on earnings between £12,571 and £50,270. If you earn more than that, you pay 40% higher rate tax on the portion above £50,270. Very high earners above £125,140 pay 45% additional rate tax.

Here’s something many people don’t realise: if you earn over £100,000, your personal allowance starts to disappear. You lose £1 of allowance for every £2 you earn above £100,000. By the time you reach £125,140, your personal allowance is completely gone. This creates an effective 60% tax rate on earnings between £100,000 and £125,140—something senior NHS managers and consultants need to watch out for.

National Insurance Contributions

National Insurance is the second major deduction. For 2025/26, you pay nothing on your first £12,570 of earnings. Between £12,571 and £50,270, you pay 8% National Insurance. Above £50,270, the rate drops to just 2%.

Unlike income tax, National Insurance is calculated on your gross pay before pension contributions are taken off. This is why your NI bill doesn’t change when you increase your pension contributions.

Read Guide: NHS Band 3 Pay 2025/26

How Tax and NI Work Together

Let’s say you’re a Band 5 nurse earning £29,970 per year. Here’s roughly what happens to your salary:

Your first £12,570 is tax-free. The remaining £17,400 gets taxed at 20%, which comes to about £3,480 in income tax. For National Insurance, you pay 8% on everything above £12,570, which works out to around £1,392. Combined, that’s roughly £4,872 in tax and NI before we even look at pension contributions.

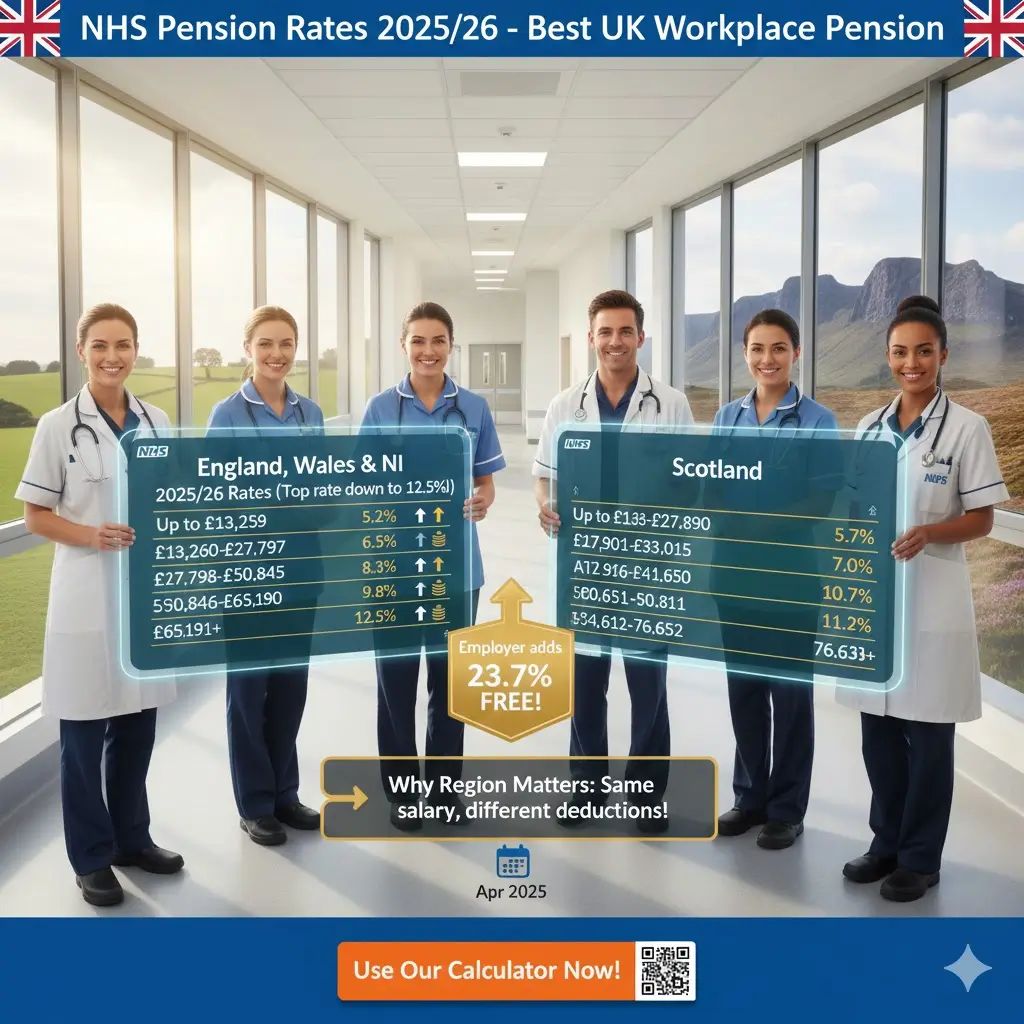

NHS Pension Contribution Rates 2025/26

NHS pension contributions are a significant deduction, but they’re also incredibly valuable. The NHS Pension Scheme is one of the best workplace pensions in the UK, with your employer contributing 23.7% on top of what you pay.

Your contribution rate depends on your pensionable pay and where you work in the UK.

Read Guide: NHS Band 2 Pay 2025/26

England, Wales and Northern Ireland Pension Tiers

From April 2025, NHS staff outside Scotland pay contributions across six tiers:

| Pensionable Pay | Contribution Rate |

| Up to £13,259 | 5.2% |

| £13,260 to £27,797 | 6.5% |

| £27,798 to £33,868 | 8.3% |

| £33,869 to £50,845 | 9.8% |

| £50,846 to £65,190 | 10.7% |

| £65,191 and above | 12.5% |

These thresholds were updated in April 2025 following the Agenda for Change pay award. The good news is that the top rate dropped from 14.7% to 12.5%, so higher earners now keep more of their salary.

Scottish NHS Pension Tiers

Scotland operates a completely different pension tier structure with eight tiers instead of six:

| Pensionable Pay | Contribution Rate |

| Up to £13,330 | 5.7% |

| £13,331 to £27,899 | 6.4% |

| £27,900 to £33,015 | 7.0% |

| £33,016 to £41,669 | 8.7% |

| £41,670 to £50,650 | 10.5% |

| £50,651 to £54,811 | 11.2% |

| £54,812 to £76,652 | 11.6% |

| £76,653 and above | 12.7% |

This is why selecting the correct region in the calculator matters—a Scottish nurse and an English nurse earning the same salary will pay different pension contributions.

How NHS Pension Contributions Affect Your Tax

Here’s something that works in your favour: NHS pension contributions are taken from your salary before income tax is calculated. This means you get automatic tax relief on your pension contributions.

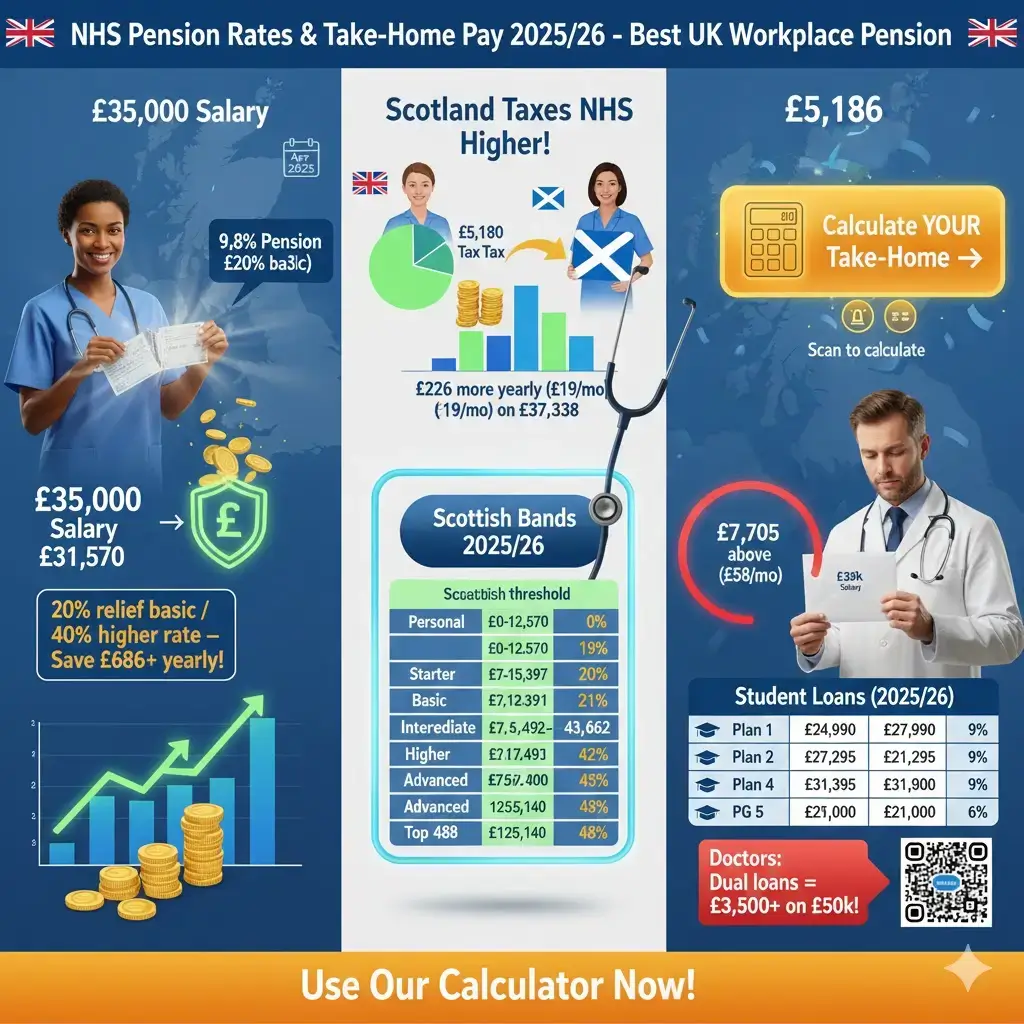

For example, if you earn £35,000 and pay 9.8% pension contributions (£3,430), your taxable income drops to £31,570. You’re effectively getting 20% back on those pension contributions—or 40% if you’re a higher rate taxpayer. This makes the NHS pension even more valuable than it first appears.

Scottish Income Tax Rates for NHS Staff

If you’re an NHS worker who lives in Scotland, you pay Scottish income tax rates regardless of where your employer is based. Scotland sets its own rates and bands, which differ significantly from the rest of the UK.

Scottish Tax Bands 2025/26

| Band | Rate | Threshold |

| Personal Allowance | 0% | Up to £12,570 |

| Starter Rate | 19% | £12,571 to £15,397 |

| Basic Rate | 20% | £15,398 to £27,491 |

| Intermediate Rate | 21% | £27,492 to £43,662 |

| Higher Rate | 42% | £43,663 to £75,000 |

| Advanced Rate | 45% | £75,001 to £125,140 |

| Top Rate | 48% | Over £125,140 |

Scotland vs England Tax Comparison

How much difference does this actually make? Let’s compare two Band 6 nurses earning £37,338—one living in England and one in Scotland.

The English nurse pays 20% on everything above their personal allowance, which comes to around £4,954 in income tax.

The Scottish nurse pays a mix of 19%, 20%, and 21% rates. They actually pay slightly less on the lower portion (19% starter rate), but then pay more on earnings above £27,492 (21% intermediate rate). Their total comes to around £5,180 in income tax.

That’s a difference of roughly £226 per year, or about £19 per month more for the Scottish nurse. The gap widens as salaries increase because Scotland’s higher rate (42%) kicks in earlier than England’s (40%) and is 2% higher.

Student Loan Repayments for NHS Workers

Many NHS staff are still paying off student loans, especially nurses who graduated after 2012 and doctors with both undergraduate and postgraduate loans. Understanding how repayments work helps you plan your finances accurately.

How Student Loan Repayments Are Calculated

Student loan repayments aren’t taken as a percentage of your whole salary. Instead, you only repay on earnings above a certain threshold. This is an important distinction—you won’t pay anything until you earn above the threshold for your plan.

Student Loan Thresholds 2025/26

| Plan | Annual Threshold | Monthly Threshold | Rate |

| Plan 1 (pre-2012) | £24,990 | £2,082 | 9% |

| Plan 2 (post-2012 England/Wales) | £27,295 | £2,274 | 9% |

| Plan 4 (Scotland) | £31,395 | £2,616 | 9% |

| Plan 5 (post-2023) | £25,000 | £2,083 | 9% |

| Postgraduate Loan | £21,000 | £1,750 | 6% |

Let’s say you’re on Plan 2 and earn £35,000. You only pay 9% on the amount above £27,295, which is £7,705. That works out to £693.45 per year, or about £58 per month—not 9% of your whole salary.

Having Multiple Student Loans

Some NHS staff, particularly doctors and advanced practitioners, have both an undergraduate loan (Plan 1, 2, 4, or 5) and a Postgraduate Loan. If this applies to you, both loans are deducted simultaneously.

Our calculator lets you add both loans to see the combined impact on your take-home pay. A doctor earning £50,000 with both Plan 2 and a Postgraduate loan could be paying over £3,500 per year in combined student loan repayments.

NHS Pay Bands and Take-Home Pay 2025/26

If you’re wondering how your pay band translates to actual money in your pocket, here’s a reference table showing estimated monthly take-home pay for each band’s starting salary.

| Band | Starting Salary | Estimated Monthly Take-Home |

| Band 2 | £24,169 | £1,720 |

| Band 3 | £25,147 | £1,780 |

| Band 4 | £26,530 | £1,860 |

| Band 5 | £29,970 | £2,050 |

| Band 6 | £37,338 | £2,480 |

| Band 7 | £46,148 | £2,950 |

| Band 8a | £53,755 | £3,350 |

| Band 8b | £65,664 | £3,950 |

| Band 8c | £78,163 | £4,550 |

| Band 8d | £93,903 | £5,250 |

| Band 9 | £107,637 | £5,850 |

Estimates based on England, standard tax code, auto-calculated pension, no student loan

How Pay Progression Affects Your Tax

As you move through pay points within your band or get promoted to a higher band, your tax situation changes in several ways.

First, you might move into a higher pension contribution tier. A Band 5 nurse at the top of their band earns £36,483, which puts them in the 9.8% pension tier instead of the 8.3% tier they started in.

Second, crossing the £50,270 threshold means paying 40% tax on earnings above that point. A Band 7 starting salary of £46,148 is below this threshold, but the top of Band 7 (£52,809) crosses into higher rate tax territory.

Planning for promotion? Use the calculator to compare your current take-home pay with what you’d earn in a higher band. The increase in gross salary doesn’t always mean as big an increase in take-home pay as you might expect.

High Income Child Benefit Charge for NHS Staff

If you earn over £60,000 and receive Child Benefit, you need to know about the High Income Child Benefit Charge (HICBC). This particularly affects NHS staff at Band 8 and above, or those with significant London weighting.

How HICBC Works

The charge was introduced to claw back Child Benefit from higher earners. From April 2024, the threshold increased from £50,000 to £60,000, which means fewer NHS staff are now affected.

Here’s how it works:

-

- If you earn under £60,000, you keep all your Child Benefit

-

- Between £60,000 and £80,000, you lose 1% of your Child Benefit for every £200 you earn above £60,000

-

- Above £80,000, you lose 100% of your Child Benefit through the charge

For example, if you earn £70,000 and receive £2,000 in annual Child Benefit, you’d lose 50% of it (£1,000) through the HICBC.

Should You Keep Claiming Child Benefit?

Even if you’ll lose most or all of the benefit through the charge, it’s often worth continuing to claim. This is because the parent receiving Child Benefit gets National Insurance credits that count toward their State Pension. These credits can be valuable, especially for parents who’ve taken career breaks.

Our calculator includes Child Benefit and shows you exactly how much the charge will be, so you can make an informed decision.

Personal Allowance Tapering for High-Earning NHS Staff

NHS consultants, senior managers, and some Band 8d/9 staff need to understand personal allowance tapering. This is one of the least understood parts of the UK tax system, but it can have a significant impact on your take-home pay.

How Tapering Works

Once your income exceeds £100,000, your £12,570 personal allowance starts to reduce. You lose £1 of allowance for every £2 you earn above £100,000.

This means:

-

- At £100,000, you have the full £12,570 allowance

-

- At £110,000, your allowance is reduced to £7,570

-

- At £120,000, your allowance is reduced to £2,570

-

- At £125,140 and above, your allowance is zero

The Hidden 60% Tax Rate

Because of tapering, earnings between £100,000 and £125,140 are effectively taxed at 60%. You pay 40% income tax, plus you lose 50p of personal allowance for every £1 earned, which adds another 20% in effective tax (40% x 50%).

This is why some NHS staff find it better to increase pension contributions or make charitable donations to keep their income below £100,000. A consultant earning £105,000 might be better off putting £5,000 extra into their pension rather than paying the effective 60% rate on that portion.

Our calculator automatically applies tapering for incomes above £100,000, so you can see the true impact on your take-home pay.

London Weighting and High Cost Area Supplements

NHS staff working in and around London receive additional pay to help with the higher cost of living. This is known as the High Cost Area Supplement (HCAS), commonly called London weighting.

HCAS Rates for 2025/26

| Area | Minimum | Maximum |

| Inner London | £5,000 | £7,097 |

| Outer London | £3,500 | £4,694 |

| Fringe | £1,258 | £1,680 |

The exact amount within these ranges depends on your trust and your pay band.

How HCAS Affects Your Deductions

London weighting is added to your gross salary before any deductions are calculated. This means it increases your taxable income and your pensionable pay.

A Band 5 nurse in Inner London earning the basic £29,970 plus £5,000 HCAS has a total income of £34,970. This higher figure is used to calculate their tax, NI, and pension contributions. While they receive more gross pay, they also pay more in deductions.

The good news is that HCAS counts toward your pension, so you’re building up a larger pension pot for retirement. Our calculator factors in HCAS when working out your take-home pay and pension contributions.

Salary Sacrifice Schemes and Tax Savings

Many NHS trusts offer salary sacrifice schemes that can save you money on tax and National Insurance. Common schemes include Cycle2Work, childcare vouchers (for existing members), and lease car arrangements.

How Salary Sacrifice Works

With salary sacrifice, you agree to give up part of your salary in exchange for a benefit. Because your salary is reduced before tax is calculated, you pay less Income Tax and National Insurance.

For example, if you join a Cycle2Work scheme for a £1,000 bike with 12-month repayments, your salary reduces by £83.33 per month. As a basic rate taxpayer, you save 20% tax plus 8% NI on this amount—a total saving of around £280 compared to buying the bike yourself.

Things to Consider

While salary sacrifice saves tax, it does reduce your pensionable pay. This means slightly lower pension contributions and slightly lower pension benefits at retirement. For most people, the tax savings outweigh this small pension reduction, but it’s worth understanding.

Our calculator includes a salary sacrifice field so you can see how these schemes affect your overall take-home pay.

NHS Pension Tax-Free Lump Sum Explained

While this calculator focuses on your take-home pay during employment, many people search for information about the tax-free lump sum they can take at retirement. Here’s a brief overview.

How the Tax-Free Lump Sum Works

When you retire from the NHS Pension Scheme, you can take up to 25% of your pension value as a tax-free lump sum. For the 2025/26 tax year, the maximum tax-free lump sum is £268,275.

In the NHS Pension Scheme, you can also “commute” some of your annual pension for an additional lump sum. This means giving up part of your yearly pension in exchange for a larger one-off payment at retirement.

This Is Different From Take-Home Pay

The pension lump sum is a retirement planning topic, separate from the monthly take-home pay calculations this tool provides. If you’re approaching retirement and want to explore your lump sum options, the NHS Business Services Authority provides a Total Reward Statement through the NHS Pensions online portal.

How NHS Monthly Pay Is Calculated

Understanding how your monthly pay is calculated helps you make sense of your payslip and spot any errors.

The Basic Formula

Your monthly take-home pay is calculated as:

(Annual Gross Salary + HCAS – Salary Sacrifice – Income Tax – National Insurance – Pension Contributions – Student Loan – HICBC) ÷ 12

Let’s work through a real example. A Band 6 nurse in England earning £37,338 with no London weighting and a Plan 2 student loan:

-

- Gross annual salary: £37,338

-

- Pension (9.8%): -£3,659

-

- Taxable income after pension and personal allowance: £21,109

-

- Income Tax (20%): -£4,222

-

- National Insurance: -£1,981

-

- Student loan (9% above £27,295): -£904

-

- Annual take-home: £26,572

-

- Monthly take-home: £2,214

When You Get Paid

Most NHS trusts pay on the last working day of each month. Your payslip is usually available a few days before payday through the Electronic Staff Record (ESR) portal.

Frequently Asked Questions

How much tax do NHS employees pay?

NHS employees pay income tax and National Insurance just like all UK workers. The amount depends on your salary, where you live, and your tax code. For 2025/26, most NHS staff pay 20% basic rate tax on earnings between £12,571 and £50,270, and 40% higher rate on earnings above this. Scottish NHS staff pay different rates ranging from 19% to 48%. A Band 5 nurse earning £29,970 typically pays around £3,480 in income tax annually. Use the calculator above to see your exact tax based on your personal circumstances.

How much of my tax goes to the NHS?

Around 20% of UK income tax revenue helps fund the NHS, making it the single largest area of government spending. However, there’s no direct link between your personal tax payment and NHS funding. All taxes go into general government revenue, and the NHS in England receives approximately £180 billion annually from various sources, including income tax, National Insurance, and VAT.

How much is £100,000 after tax in the UK?

A £100,000 salary in England leaves you with approximately £67,500 net take-home pay annually, which works out to around £5,625 monthly after tax, NI, and NHS pension contributions. However, this varies based on pension contributions, student loans, and region. Scottish residents pay slightly more tax due to higher rates above £43,662. At exactly £100,000, you keep your full personal allowance—but earning even £1 more triggers tapering, making salaries just above £100,000 particularly tax-inefficient.

Who pays 40% tax in the UK?

You pay 40% higher tax rate on income above £50,270 in 2025/26 if you live in England, Wales, or Northern Ireland. In Scotland, the higher rate of 42% applies from £43,663. For NHS staff, this typically affects Band 7 and above, especially those with London weighting or at higher pay points. Remember, the 40% rate only applies to earnings above the threshold—not your entire salary.

Is £23,000 a good salary in the UK after tax?

A £23,000 gross salary provides approximately £19,400 net take-home annually, which is around £1,616 monthly after tax and NI, assuming no pension contributions. For NHS staff, pension contributions reduce this further. This is below the UK median full-time salary of roughly £35,000 and may be challenging in high-cost areas like London. It’s roughly equivalent to NHS Band 2 at the lower pay points.

How is NHS monthly pay calculated?

NHS monthly pay is calculated by dividing your annual salary by 12, then subtracting deductions. Deductions include Income Tax, National Insurance, NHS Pension contributions (5.2%-12.5% depending on salary), and any student loan repayments. For example, a Band 5 nurse earning £29,970 annually receives £2,497.50 gross monthly, with approximately £450 deducted for tax and NI and £250 for pension, leaving around £1,800 net take-home.

What is the NHS pension contribution rate for 2025/26?

NHS pension contributions range from 5.2% to 12.5% in England, Wales, and Northern Ireland based on your pensionable pay. Scotland has different rates from 5.7% to 12.7% across eight tiers. The rates and thresholds were updated from April 2025 following the 3.6% Agenda for Change pay award. Contributions are tax-efficient because they’re deducted before income tax is calculated, giving you automatic tax relief.

Can I opt out of the NHS pension?

Yes, you can opt out of the NHS Pension Scheme, but it’s rarely advisable. The scheme includes employer contributions of 23.7%—effectively more than doubling your pension savings. Opting out increases your take-home pay now but significantly reduces your retirement income. Our calculator includes an “opted out” option so you can see the difference and make an informed choice.

How do I know my NHS pension tier?

Your pension tier is determined by your actual pensionable pay, not your whole-time equivalent salary. Check your payslip for your contribution percentage, or use our calculator which auto-calculates your tier based on your salary. Part-time staff pay is based on their actual earnings, which often places them in a lower tier than their full-time equivalent band would suggest.

Does London weighting affect my pension contributions?

Yes, High Cost Area Supplements are pensionable, meaning they increase both your pension contributions and your pension benefits. A nurse receiving Inner London weighting of £5,000 will have this added to their pensionable pay, potentially moving them into a higher contribution tier. The upside is that you’re building a larger pension for retirement.

A Note on Accuracy

This NHS tax calculator provides estimates based on the official 2025/26 thresholds from HMRC and NHS Employers. While we strive for accuracy, your actual take-home pay may differ slightly due to factors like tax code adjustments, additional allowances, or mid-year changes.

For official figures, always check your payslip through the Electronic Staff Record and compare it with HMRC’s own income tax calculator. If you notice significant discrepancies between this calculator and your payslip, speak to your trust’s payroll department.

We update this calculator each April when new tax thresholds and NHS pension rates come into effect. Bookmark this page to check your take-home pay whenever your circumstances change—whether that’s a promotion, a student loan threshold change, or a new tax year