Smart NHS Pension Calculator 2026/27

Stop guessing your retirement income. Our free NHS Pension Calculator is updated for 2026/27, covering everything others miss. Calculate 1995, 2008, and 2015 scheme benefits instantly. Compare McCloud Remedy options, check Annual Allowance charges, explore partial retirement, and see your tax-free lump sum with the £268,275 LSA cap applied. Works for England, Scotland, and Northern Ireland. Whether you are an Officer or GP Practitioner, get accurate pension projections in seconds without spreadsheets or waiting for official estimates.

📋 How to Get Your Pension Data

- Log into ESR Self Service or NHS Pensions Online

- Access your Annual Benefit Statement (ABS)

- Find your pensionable pay and years of service

- Enter these values below for accurate results

From 1 October 2022, your contribution rate is based on actual reduced pay, not your full salary. However, your pension benefits still accrue based on your deemed (full) pay.

📊 Your Contribution Rate 2026/27

▼The Annual Allowance is the maximum amount your pension can grow in a tax year before you face tax charges. For 2026/27, the standard limit is £60,000.

If your adjusted income exceeds £260,000, your AA is reduced by £1 for every £2 over the threshold, down to a minimum of £10,000.

You can elect for the NHS Pension Scheme to pay the tax charge from your pension benefits.

Scheme Pays Calculation

You may face a tax charge. Consider using Scheme Pays.

Draw between 20% and 80% of your pension while continuing to work. You must reduce your pay by at least 10%.

Purchase up to £8,946.24 per year (2026/27 limit).

£1,000 purchase costs £800 (basic rate) or £600 (higher rate).

🛡️ Death Benefits

▼| Age | Annual Pension | Reduction | Monthly Net* |

|---|

⚠️ Important Disclaimer

This calculator provides estimates for illustrative purposes only.

- Early retirement uses approximate 5% per year reductions

- 2015 scheme projections assume CPI + 1.5% revaluation

- Use the official NHS BSA McCloud Remedy Benefits Illustrator for personalised figures

- Annual Allowance calculations should be verified using NHS Employers Ready Reckoner

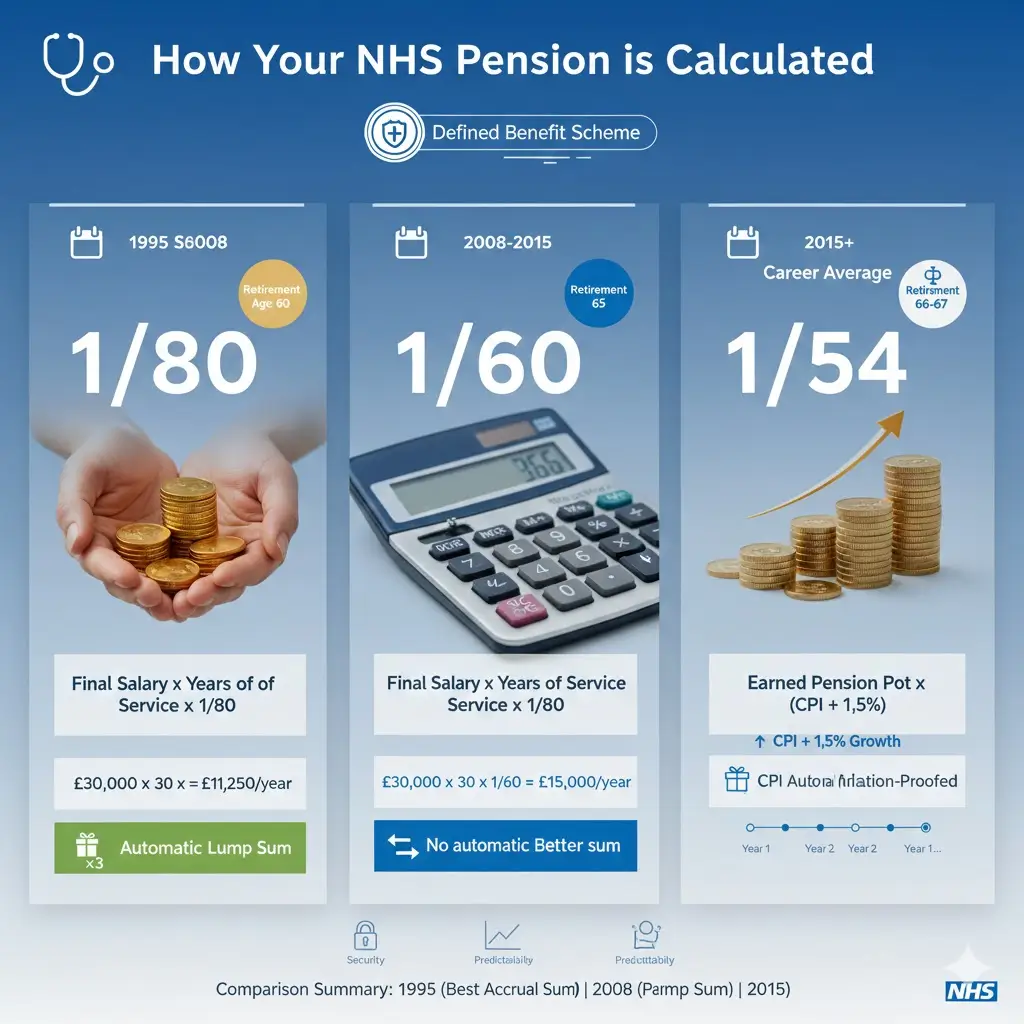

How is Your NHS Pension Calculated?

Your NHS pension is worked out using a simple formula. The exact formula depends on which scheme you belong to. There are three NHS pension schemes, and each one calculates your pension differently.

The NHS pension is a defined benefit scheme. This means your pension is based on a set formula, not on how investments perform. This makes it very secure and predictable.

The Three NHS Pension Formulas

1995 Section Formula

If you joined the NHS before March 2008, you may have years in the 1995 Section. This scheme gives you:

- 1/80th of your final salary for each year you worked

- Plus an automatic tax-free lump sum worth 3 times your yearly pension

- A retirement age of 60

How to calculate it:

Your Final Salary × Years Worked ÷ 80 = Your Yearly Pension

For example, if your final salary is £40,000 and you worked for 20 years:

£40,000 × 20 ÷ 80 = £10,000 per year

Your automatic lump sum would be £10,000 × 3 = £30,000

2008 Section Formula

If you joined between April 2008 and March 2015, you may have years in the 2008 Section. This scheme gives you:

- 1/60th of your best salary for each year you worked

- No automatic lump sum (but you can swap pension for cash)

- A retirement age of 65

How to calculate it:

Your Best Salary × Years Worked ÷ 60 = Your Yearly Pension

Using the same example of £40,000 salary and 20 years:

£40,000 × 20 ÷ 60 = £13,333 per year

The 2008 Section builds up pension faster (1/60th vs 1/80th), but you retire later and get no automatic lump sum.

2015 Scheme Formula (Career Average)

Everyone now builds up pension in the 2015 Scheme. This is different from the older schemes because it uses your career average earnings, not your final salary.

- 1/54th of your pensionable pay each year

- Your pension pot grows by CPI + 1.5% every year

- Retirement age is your State Pension Age (currently 66-67)

How to calculate it:

Each Year’s Salary ÷ 54 = Pension Earned That Year

If you earn £30,000 in one year:

£30,000 ÷ 54 = £556 added to your pension pot

This £556 then grows each year by inflation plus 1.5%. Over 30 years, this growth adds up significantly.

How is Final Salary Calculated?

For the 1995 and 2008 Sections, your “final salary” is not simply your last pay cheque. Here is how it works:

1995 Section: Your final salary is the higher of:

- Your pay for the last 365 days, OR

- The best of your last 3 years’ pay

2008 Section: Your final salary is:

- The average of your best 3 consecutive years’ pay in your last 10 years

This protects you if your pay drops before retirement. Your pension is based on your best earnings, not necessarily your very last salary.

Understanding Each NHS Pension Scheme

For the 1995 and 2008 Sections, your “final salary” is not simply your last pay cheque. Here is how it works:

1995 Section: Your final salary is the higher of:

- Your pay for the last 365 days, OR

- The best of your last 3 years’ pay

2008 Section: Your final salary is:

- The average of your best 3 consecutive years’ pay in your last 10 years

This protects you if your pay drops before retirement. Your pension is based on your best earnings, not necessarily your very last salary.

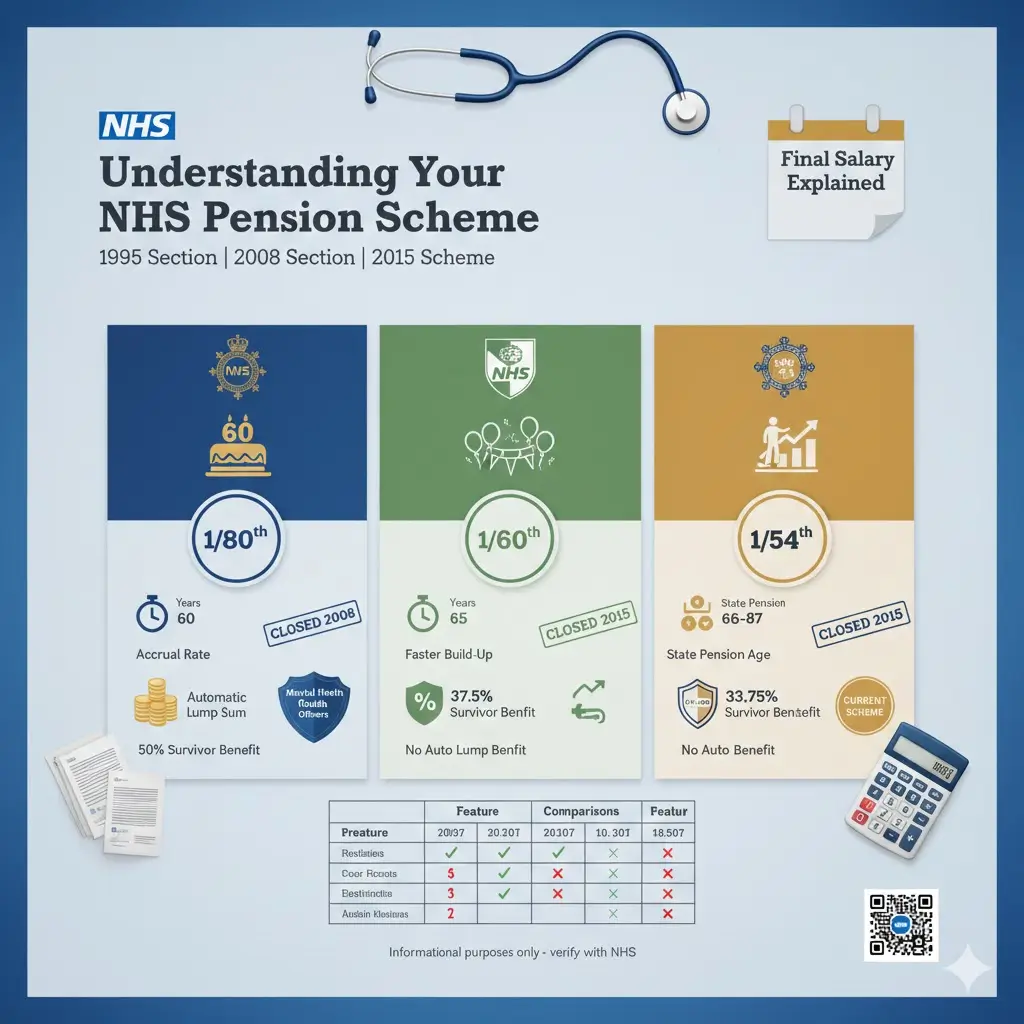

The 1995 Section Explained

The 1995 Section is the oldest part of the NHS pension. It closed to new members in 2008, but many long-serving NHS staff still have years in this scheme.

Key Features:

Feature | What You Get |

How pension builds up | 1/80th of final salary per year |

Normal retirement age | 60 |

Automatic lump sum | Yes – 3 times your yearly pension |

Survivor pension | 50% of your pension goes to your spouse |

Early retirement | From age 55 with reductions |

Best thing about it: You can retire at 60 with full pension, and you automatically get a tax-free lump sum without giving up any pension.

Mental Health Officers: If you work as a Mental Health Officer in Scotland, your retirement age is 55, not 60.

The 2008 Section Explained

The 2008 Section was introduced for people who joined between April 2008 and March 2015. It builds pension faster than the 1995 Section but has no automatic lump sum.

Key Features:

Feature | What You Get |

How pension builds up | 1/60th of reckonable pay per year |

Normal retirement age | 65 |

Automatic lump sum | No (you must swap pension to get cash) |

Survivor pension | 37.5% of your pension goes to your spouse |

Early retirement | From age 55 with reductions |

Best thing about it: Faster pension build-up means more income in retirement if you work full career.

The 2015 Scheme Explained

The 2015 Scheme is the current scheme for all NHS staff. From April 2022, everyone moved into this scheme.

Key Features:

Feature | What You Get |

How pension builds up | 1/54th of each year’s pay |

Normal retirement age | State Pension Age (currently 66-67) |

Automatic lump sum | No (you must swap pension to get cash) |

Survivor pension | 33.75% of your pension goes to your spouse |

Yearly revaluation | CPI + 1.5% (protects against inflation) |

Best thing about it: Your pension grows each year with inflation plus 1.5%, even when you do not get a pay rise. This protects your pension against rising prices.

Comparing All Three Schemes

Feature | 1995 Section | 2008 Section | 2015 Scheme |

Pension per year worked | 1/80th | 1/60th | 1/54th |

Retirement age | 60 | 65 | State Pension Age |

Automatic cash lump sum | Yes (3× pension) | No | No |

Spouse gets if you die | 50% | 37.5% | 33.75% |

Based on | Final salary | Best 3 of last 10 years | Career average |

Still open | No | No | Yes |

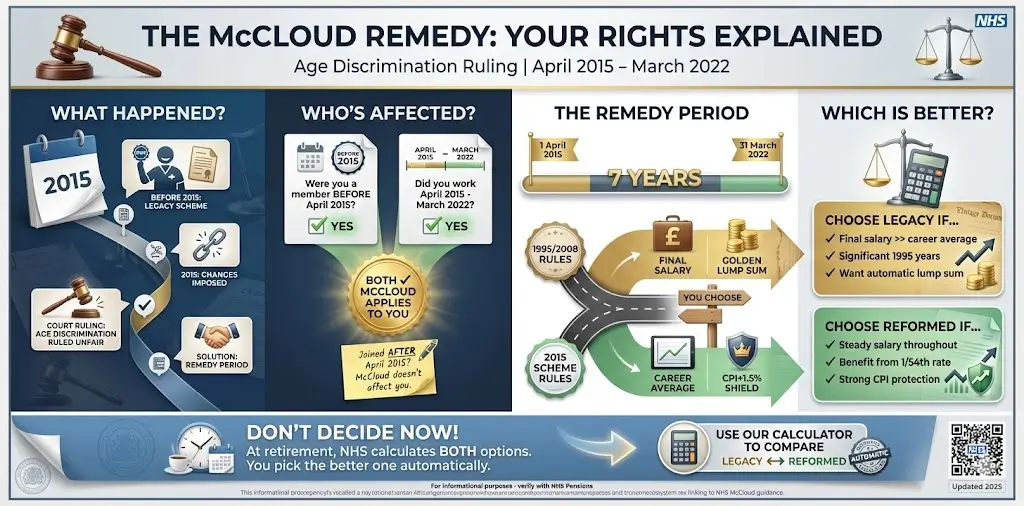

The McCloud Remedy: What You Need to Know

What is the McCloud Remedy?

In 2015, the government moved everyone into the new 2015 pension scheme. But this was unfair to older workers who had less time to adjust their retirement plans.

The courts agreed this was age discrimination. The McCloud Remedy is the fix for this problem.

Who Does McCloud Affect?

You are affected by McCloud if:

- You were a member of the NHS pension before April 2015, AND

- You worked in the NHS between 1 April 2015 and 31 March 2022 (the “remedy period”)

If you only joined the NHS after April 2015, McCloud does not affect you.

How Does the Remedy Work?

For the 7-year remedy period (April 2015 to March 2022), you get to choose which scheme rules apply:

Option 1: Legacy Scheme Rules Your pension for those years is calculated using the 1995 or 2008 rules (whichever you were in before).

Option 2: Reformed Scheme Rules Your pension for those years is calculated using the 2015 scheme rules.

You will pick whichever option gives you more pension. You do not need to decide now. When you retire, the NHS Pension Scheme will calculate both options and let you choose the better one.

Which Option is Usually Better?

Legacy scheme is usually better if:

- Your final salary is much higher than your career average

- You have significant years in the 1995 Section (to get the automatic lump sum)

2015 scheme is usually better if:

- Your salary stayed fairly steady throughout your career

- The higher 1/54th accrual rate works in your favour

Our calculator lets you toggle between Legacy and Reformed rules to see the difference.

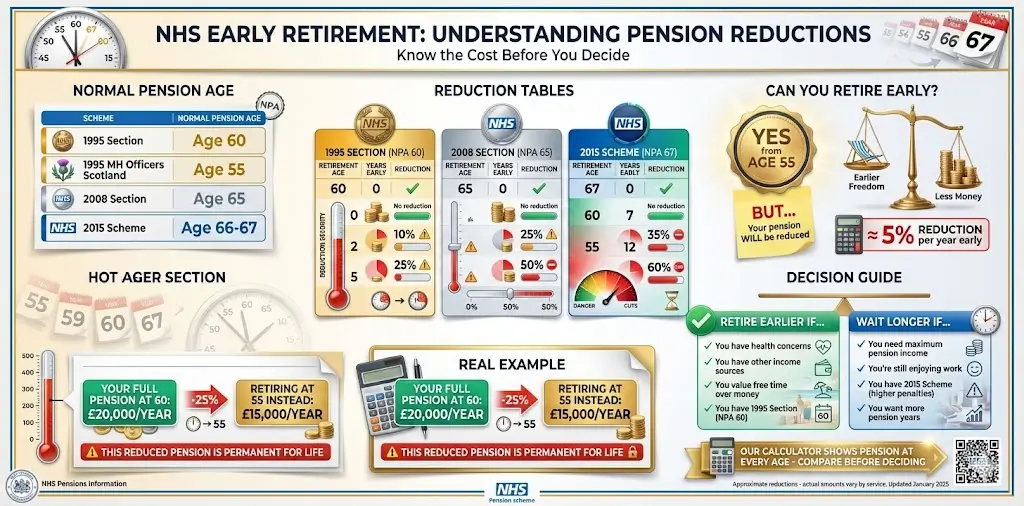

NHS Early Retirement: Understanding Pension Reductions

What is Normal Pension Age?

Your Normal Pension Age (NPA) is the age when you can take your full pension with no reductions.

Scheme | Normal Pension Age |

1995 Section | 60 |

1995 Section (Mental Health Officers in Scotland) | 55 |

2008 Section | 65 |

2015 Scheme | State Pension Age (66-67) |

Can You Retire Early?

Yes. You can take your NHS pension from age 55, but your pension will be reduced.

The reduction is roughly 5% for each year you retire before your Normal Pension Age. This is called an actuarial reduction. It happens because you will receive your pension for more years.

How Much Will You Lose Retiring Early?

Here is how early retirement reductions work:

1995 Section (NPA 60):

Retirement Age | Years Early | Approximate Reduction |

60 | 0 | No reduction |

58 | 2 | 10% less |

55 | 5 | 25% less |

2008 Section (NPA 65):

Retirement Age | Years Early | Approximate Reduction |

65 | 0 | No reduction |

60 | 5 | 25% less |

55 | 10 | 50% less |

2015 Scheme (NPA 67):

Retirement Age | Years Early | Approximate Reduction |

67 | 0 | No reduction |

60 | 7 | 35% less |

55 | 12 | 60% less |

Example: If your full pension would be £20,000 per year at age 60, but you retire at 55 from the 1995 Section, you would get:

£20,000 – 25% = £15,000 per year

This reduced pension is paid for life. It does not go back up when you reach 60.

What is the Best Age to Retire?

There is no single “best” age. It depends on your situation:

Consider retiring earlier if:

- You have health concerns

- You have other income sources

- You value free time over money

- You have 1995 Section membership (NPA 60)

Consider waiting longer if:

- You need maximum pension income

- You are still enjoying work

- You have 2015 Scheme membership (higher NPA means bigger reductions for early retirement)

- You want to build up more pension years

Our calculator shows you pension amounts at different retirement ages so you can compare.

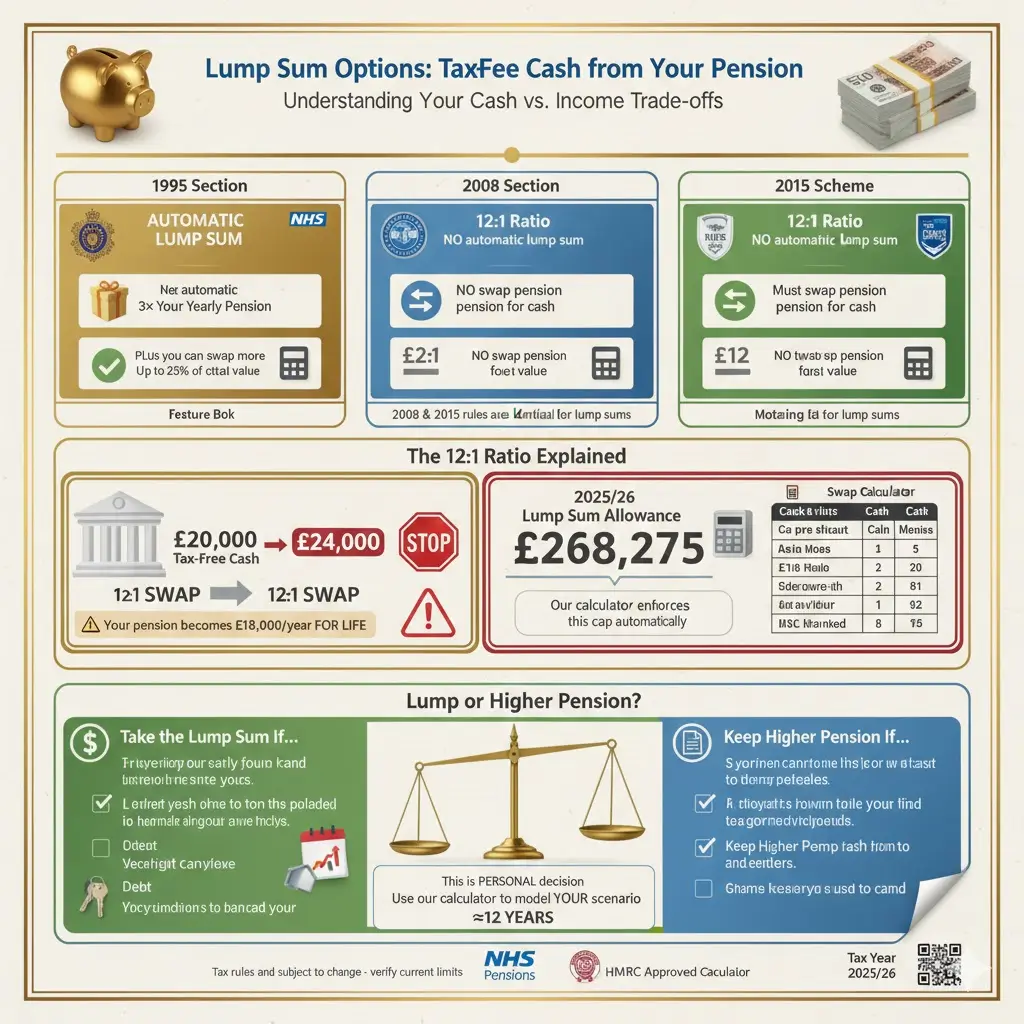

Lump Sum Options: Tax-Free Cash from Your Pension

How Lump Sum Works

When you retire, you can take some of your pension as tax-free cash. How this works depends on your scheme.

1995 Section:

- You automatically get a lump sum worth 3 times your yearly pension

- You can also swap some pension for extra cash (up to 25% of total value)

2008 Section and 2015 Scheme:

- No automatic lump sum

- You can swap pension for cash at a 12:1 ratio

- Maximum is 25% of your pension’s capital value

What is the 12:1 Commutation Ratio?

If you want cash from the 2008 or 2015 schemes, you must give up some pension. For every £1 of yearly pension you give up, you get £12 as a lump sum.

Example: You give up £2,000 of yearly pension You get £2,000 × 12 = £24,000 as cash

Your pension then becomes £2,000 less per year for life.

The £268,275 Lump Sum Cap

Since 2024, there is a cap on how much tax-free cash you can take from all your pensions combined. This is called the Lump Sum Allowance (LSA).

For 2026/27, the cap is £268,275.

If your total tax-free cash would exceed this, the excess is taxed as income.

Our calculator automatically enforces this cap and warns you if you reach it.

Should You Take Lump Sum or Keep Higher Pension?

This is a personal decision. Here are things to consider:

Take the lump sum if:

- You need cash for something specific (pay off mortgage, clear debts)

- You have concerns about your health or life expectancy

- You have no other savings

Keep higher pension if:

- You do not have an immediate need for cash

- You expect to live a long life (the breakeven point is roughly 12 years)

- You want maximum guaranteed income

The 12:1 ratio is generally considered not very generous. If you live more than 12 years after retirement, you would have been better off keeping the higher pension.

NHS Pension Contribution Rates 2026/27

How Much Do You Pay?

Your pension contribution depends on how much you earn. The more you earn, the higher your contribution rate.

Your contribution is taken from your salary before tax, so you get tax relief automatically.

England and Wales Contribution Rates

These rates apply from April 2025:

Your Pensionable Pay | Contribution Rate |

Up to £13,259 | 5.2% |

£13,260 to £27,797 | 6.5% |

£27,798 to £33,868 | 8.3% |

£33,869 to £50,845 | 9.8% |

£50,846 to £65,190 | 10.7% |

£65,191 and above | 12.5% |

Example: If you earn £35,000, your contribution rate is 9.8%. Your yearly contribution: £35,000 × 9.8% = £3,430 Your monthly contribution: £3,430 ÷ 12 = £286

Scottish NHS Pension Contribution Rates

Scotland has different contribution rates:

Your Pensionable Pay | Contribution Rate |

Up to £13,330 | 5.7% |

£13,331 to £26,762 | 6.4% |

£26,763 to £31,669 | 7.0% |

£31,670 to £39,734 | 8.7% |

£39,735 to £41,669 | 9.8% |

£41,670 to £50,650 | 10.5% |

£50,651 to £54,811 | 11.2% |

£54,812 to £76,652 | 11.6% |

£76,653 and above | 12.7% |

Northern Ireland (HSC) Contribution Rates

Northern Ireland also has different rates:

Your Pensionable Pay | Contribution Rate |

Up to £13,259 | 5.2% |

£13,260 to £26,831 | 6.7% |

£26,832 to £32,691 | 8.5% |

£32,692 to £49,078 | 10.0% |

£49,079 to £62,924 | 10.9% |

£62,925 and above | 12.7% |

What About Employer Contributions?

Your employer also pays into your pension:

- England and Wales: 20.6% of your pensionable pay

- Scotland: 22.5% of your pensionable pay

This makes the NHS pension extremely valuable. For every £1 you put in, your employer puts in roughly £2-3.

Related Guide: NHS Pension Employer Contributions

If You Are on Reduced Pay

From October 2022, if you are on reduced pay (maternity leave, sick leave), your contribution rate is based on your actual reduced pay, not your full salary.

This means you pay less during absence. However, your pension benefits still build up as if you were on full pay. This is a good deal for staff on leave.

Annual Allowance: Avoiding Pension Tax Charges

From October 2022, if you are on reduced pay (maternity leave, sick leave), your contribution rate is based on your actual reduced pay, not your full salary.

This means you pay less during absence. However, your pension benefits still build up as if you were on full pay. This is a good deal for staff on leave.

What is Annual Allowance?

The Annual Allowance is the maximum amount your pension can grow in one tax year before you face extra tax charges.

For 2026/27, the standard Annual Allowance is £60,000.

This sounds like a lot, but high-earning NHS staff, especially doctors and senior managers, can exceed it.

How is Pension Growth Calculated?

HMRC calculates your pension growth using this formula:

Step 1: Opening Value = (Your pension at start of tax year × 16) + any lump sum

Step 2: Closing Value = (Your pension at end of tax year × 16) + any lump sum

Step 3: Pension Input Amount = Closing Value – (Opening Value × (1 + CPI%))

If your Pension Input Amount exceeds £60,000, you may face a tax charge.

Tapered Annual Allowance for High Earners

If your “adjusted income” exceeds £260,000, your Annual Allowance is reduced.

For every £2 you earn over £260,000, your allowance drops by £1.

The minimum Annual Allowance is £10,000.

Example: If your adjusted income is £300,000:

- You are £40,000 over the threshold

- Your allowance drops by £40,000 ÷ 2 = £20,000

- Your Annual Allowance is £60,000 – £20,000 = £40,000

What is Scheme Pays?

If you exceed your Annual Allowance, you can ask the NHS Pension Scheme to pay the tax charge for you. This is called Scheme Pays.

The pension scheme pays the tax, but your future pension is reduced to cover the cost. It is like borrowing from your future self.

Scheme Pays can be useful if you do not have cash to pay the tax bill upfront.

Our Annual Allowance calculator helps you check if you might exceed the limit.

NHS Pension Calculator Examples

Example 1: Band 5 Nurse, 2015 Scheme Only

Your Details:

- Current salary: £31,049

- Years in 2015 Scheme: 10

- Retirement age: 67 (State Pension Age)

Calculation: £31,049 × 10 ÷ 54 = £5,749 per year

This is your pension at today’s values. With revaluation of 4% per year over 20 more working years, your pension could grow to approximately £12,600 per year.

No automatic lump sum, but you could swap some pension for cash at retirement.

Example 2: Band 7 with Split Scheme Membership

Your Details:

- Final salary: £54,710

- 1995 Section years: 15

- 2015 Scheme years: 10

- McCloud remedy years: 7 (choosing Legacy rules)

- Retirement age: 60

1995 Section Calculation (including McCloud years): £54,710 × 22 ÷ 80 = £15,045 per year

Automatic Lump Sum: £15,045 × 3 = £45,135 tax-free cash

2015 Scheme Calculation: £54,710 × 10 ÷ 54 = £10,131 per year (before revaluation)

Note: The 2015 portion would have early retirement reductions if taken at 60 (because NPA is 67).

Total at age 60: Approximately £22,000 – £25,000 per year depending on revaluation and reductions.

Example 3: Part-Time Worker

Your Details:

- Full-time equivalent salary: £40,000

- Working 60% of full-time hours

- Actual salary: £24,000

- Years of service: 15

Your pension is based on actual pay: £24,000 × 15 ÷ 54 = £6,667 per year

Part-time service counts fully for pension purposes, but the pension amount is based on actual earnings.

Partial Retirement: Draw Pension While Still Working

What is Partial Retirement?

Partial retirement lets you take some of your pension while continuing to work. You reduce your hours and draw part of your pension to top up your income.

This is also called “flexible retirement” or “drawdown”.

How Does It Work?

You can draw between 20% and 80% of your built-up pension. The part you do not draw stays in the scheme and continues to grow.

Requirements:

- You must be at least 55

- You must reduce your pensionable pay by at least

Example of Partial Retirement

Your Details:

- Current salary: £45,000

- Built-up pension: £20,000 per year

- Age: 58 (NPA 60)

- You want to work 60% of current hours

What You Get:

- Reduced salary: £45,000 × 60% = £27,000 per year

- You draw 50% of pension: £20,000 × 50% = £10,000

- But you are 2 years early (NPA 60), so 10% reduction applies

- Actual pension income: £10,000 × 90% = £9,000 per year

Total Income: £27,000 + £9,000 = £36,000 per year

Plus you keep building up more pension on your reduced hours.

Reserved for later: The other 50% (£10,000) stays in the scheme, growing until you fully retire.

Buying Extra NHS Pension

Can You Buy More Pension?

Yes. The NHS pension scheme lets you purchase Additional Pension to boost your retirement income.

For 2025/27, you can buy up to £8,946.24 of extra yearly pension.

How Much Does It Cost?

The cost depends on your age. The younger you are, the cheaper it is because your extra pension has more years to be paid.

Rough cost guide:

Your Age | Cost per £1,000 Extra Pension |

30 | Around £12,000 |

40 | Around £15,000 |

50 | Around £18,000 |

60 | Around £22,000 |

You can pay:

- As a lump sum, or

- Through monthly payments from your salary

Is It Worth Buying Extra Pension?

Advantages:

- You get tax relief on contributions (effectively 20-40% discount)

- Your extra pension is guaranteed for life

- It is inflation-protected

Disadvantages:

- Money is locked away until retirement

- If you die early, you may not get value back

- Returns depend on how long you live

Our Additional Pension calculator helps you estimate the cost and breakeven point.

Related Guide: NHS Pension Contributions Rates 2026/27

Common NHS Pension Questions Answered

How many years do you need for a full NHS pension?

There is no set number of years for a “full” pension. Your pension is based on your actual years of service and pay. The more years you work, the bigger your pension.

In the old days, the 1995 Section had a maximum of 40 years and the 2008 Section had 45 years. But the 2015 Scheme has no limit on years you can build up.

So there is no target number you need to hit. Every year of service adds to your pension.

What happens to your NHS pension if you leave the NHS?

If you leave the NHS before retirement, your pension is preserved. This is called a deferred pension.

Your pension stays in the scheme and is revalued each year to keep pace with inflation. When you reach your Normal Pension Age, you can claim it.

You can also:

- Transfer your NHS pension to another scheme (rarely a good idea)

- Take it early from age 55 with reductions

- Leave it until your NPA for full value

If you have less than 2 years service, you may get a refund of contributions instead of a pension.

Are NHS pensions paid for life?

Yes. Your NHS pension is paid every month for the rest of your life, no matter how long you live.

It is also index-linked, meaning it goes up each year with inflation (CPI). This protects your buying power as prices rise.

If you die, a percentage goes to your spouse or civil partner:

- 1995 Section: 50% of your pension

- 2008 Section: 37.5% of your pension

- 2015 Scheme: 33.75% of your pension

Why do NHS staff not get full state pension?

NHS staff can get the full State Pension if they have 35 qualifying years of National Insurance contributions.

However, some NHS staff who were “contracted out” before 2016 may get a lower State Pension. This is because part of their additional state pension was provided by the NHS pension instead.

This shows as a COPE deduction (Contracted Out Pension Equivalent) on your State Pension forecast. It is not money taken from you – it is pension already provided through NHS.

If you worked in the NHS before 2016, check your State Pension forecast to see if COPE affects you.

What is the 70% rule for pension?

The 70% rule is a general retirement guideline. It suggests you need about 70% of your pre-retirement income to maintain your lifestyle in retirement.

For NHS staff, this might come from:

- Your NHS pension

- The State Pension

- Other savings (ISAs, private pensions)

Your NHS pension alone may provide 20-50% of your final salary, depending on your years of service. The State Pension adds more. You may need additional savings to reach 70%.

Our calculator helps you see what percentage of your salary your NHS pension will provide.

Should I take a lump sum or keep higher monthly pension?

This depends on your personal situation.

The maths: The NHS commutation rate is 12:1. This means if you take a £12,000 lump sum instead of £1,000 per year pension, the breakeven point is 12 years. If you live more than 12 years after retirement, you would have been better off keeping the higher pension.

Take lump sum if:

- You need cash now (pay off mortgage, buy something specific)

- You have health concerns about longevity

- You have no other savings

Keep higher pension if:

- You expect to live a long retirement

- You do not have an immediate need for cash

- You want maximum guaranteed income

Remember, the 1995 Section gives you an automatic lump sum without reducing your pension. You only face this choice for additional commutation or for 2008/2015 schemes.

How much will I lose if I take my pension at 55?

Early retirement reductions are approximately 5% per year before your Normal Pension Age.

1995 Section (NPA 60): Retiring at 55 = 5 years early = approximately 25% reduction

2008 Section (NPA 65): Retiring at 55 = 10 years early = approximately 50% reduction

2015 Scheme (NPA 67): Retiring at 55 = 12 years early = approximately 60% reduction

Example: If your full pension would be £20,000 at NPA:

- 1995 Section at 55: £20,000 × 75% = £15,000 per year

- 2008 Section at 55: £20,000 × 50% = £10,000 per year

- 2015 Scheme at 55: £20,000 × 40% = £8,000 per year

These reductions are permanent. Your pension does not go up when you reach NPA.

Death Benefits: What Your Family Gets

Lump Sum Death Grant

If you die while still working in the NHS, your family receives a lump sum death grant. This is typically 2 times your pensionable pay.

Example: If your salary is £40,000, your family would receive £80,000.

This is paid to whoever you nominate (or your estate if you have not nominated anyone).

Survivor Pensions

Your spouse, civil partner, or qualifying partner receives a pension for their lifetime:

Scheme | Survivor Gets |

1995 Section | 50% of your pension |

2008 Section | 37.5% of your pension |

2015 Scheme | 33.75% of your pension |

Example: If your pension was £20,000 per year:

- 1995 Section: Spouse gets £10,000 per year for life

- 2008 Section: Spouse gets £7,500 per year for life

- 2015 Scheme: Spouse gets £6,750 per year for life

Children's Pensions

If you have dependent children, they may also receive a pension until they reach adulthood or finish full-time education.

Important Disclaimer

This calculator provides estimates for illustrative purposes only. Your actual pension may be different.

Please note:

- Early retirement reductions shown use approximate 5% per year factors. The official NHS BSA calculations use actuarial tables that vary by exact age and scheme

- 2015 scheme projections assume CPI + 1.5% revaluation, which may vary in practice

- For McCloud-affected members, we recommend also using the official NHS BSA McCloud Remedy Benefits Illustrator

- Annual Allowance calculations should be verified using the NHS Employers Ready Reckoner

Official Resources

For binding pension figures, always contact NHS Pensions or use these official sources:

- NHS Pensions Online – Access your Annual Benefit Statement

- NHS BSA Member Hub – Request official pension estimates

- NHS BSA McCloud Remedy Benefits Illustrator – Compare legacy vs reformed options

- NHS BSA Early Retirement Calculator – Official reduction factors

- NHS Employers Ready Reckoner – Annual Allowance calculations

- SPPA – For Scottish NHS pension members